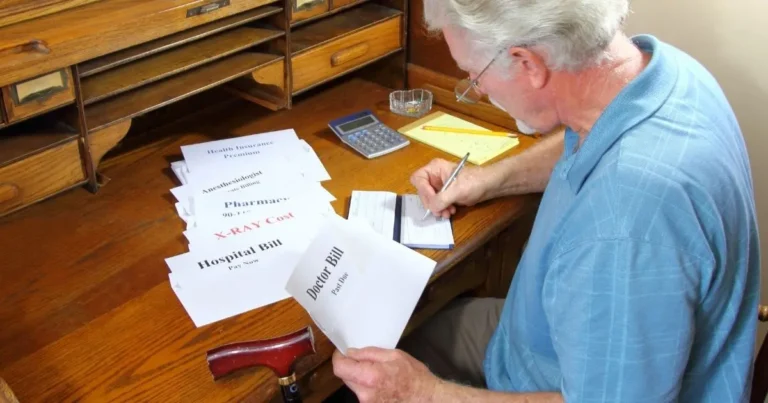

How will my settlement be taxed after a personal injury, worker’s compensation, or employment case?~2 min read

Our clients who receive settlement payments often have questions about how these settlement payments will be taxed, or if they will be taxed at all. While our firm does not practice tax law, and we always advise our clients to discuss these matters with an experienced accountant or tax preparation service, this article discusses the general rules for taxation of settlement payments in the areas of law our firm practices.

Taxation in personal injury cases is simple: you will not pay taxes on a personal injury settlement in almost all circumstances. The IRS does not tax settlement money for personal injury claims because these funds are intended to make an injured person whole again. In other words, the federal government does not consider settlement of personal injury claims to be income because the injured person has not gained anything, they have been brought back to the position they were at before they were injured.

Similarly, worker’s compensation settlements, generally called lump sum settlements, are also not taxable. The logic for this is the same as for personal injury settlements, an injured worker is being made whole by these settlements, not receiving income from these settlements. One question worker’s compensation clients may have is whether their weekly benefit checks will be taxed as wages. The answer is clear, such benefits are specifically excluded from taxation by the IRS tax code. One situation where an injured worker may still have a taxable event is if they are working on a reduced schedule and are receiving benefits for the reduction of hours worked. There, the employee would be taxed and receive a W2 for the hours they worked, but would not be taxed on the worker’s compensation benefits.

Finally, in the employment context, settlement payments are generally based on two things, lost wages and compensatory damages for illegal conduct by the employer. In contrast to the other types of settlements, according to the IRS, these types of settlements are taxable as income. Further, the employee must claim the full settlement amount on their taxes including the portion paid to their attorney. In certain circumstances, however, this attorney’s fee portion can be a deduction.

As always, it is important to verify whether you owe any taxes with a certified public accountant (CPA), and this blog is not intended to substitute for the advice of an experienced accountant. If you have specific tax questions, it is important to speak with a CPA of your own choosing.

If you have been injured due to a motor vehicle, motorcycle collisions, falls, work accident, or feel you have been wrongfully terminated, the Civil Litigation Attorneys at Parnell, Michels & McKay are ready to meet with you. Please contact our team of experienced attorneys today.

Our firm blends advocacy oriented practice with effective practical solutions for all our clients in Londonderry, N. Woodstock, and throughout New Hampshire. The attorneys at Parnell, Michels & McKay provide effective representation and counseling to assist our clients facing legal questions. We simplify the process so our clients can understand and are able to participate as partners in the resolution.

Our practice includes personal injury law such as motor vehicle accidents, falls, dog bites, workers compensation, social security disability, and other injuries.

We also practice family law, including divorce, post-divorce, unwed custody and property division, and collaborative divorce, and have extensive experience in bankruptcy, probate, boundary disputes, estate planning, corporate formation and other real estate litigation.